Through the Downturns: Casino Stocks' Dividend Track Records in Economic Crises

Through the Downturns: Casino Stocks' Dividend Track Records in Economic Crises

Economic Shocks Hit the Gaming Sector Hard

Casino stocks often ride high on booming tourism and disposable income, but when recessions strike, revenue plummets fast since gamblers cut back on trips and bets; data from past crises reveals how major players like Las Vegas Sands (LVS), MGM Resorts (MGM), and Wynn Resorts (WYNN) navigated dividend policies amid sharp declines in gross gaming revenue (GGR). Observers note that while the industry rebounds resiliently, dividends serve as a litmus test for financial health, with some companies suspending payouts entirely while others trimmed them strategically to preserve cash. Take the global financial crisis of 2008, when U.S. casino revenues fell 10% year-over-year according to Nevada Gaming Control Board reports, forcing executives to rethink shareholder returns.

And yet, not every operator fared the same; Boyd Gaming, for instance, maintained a modest dividend through 2008 before suspending it in 2009 as debt mounted, whereas regional players like Penn National Gaming (now Penn Entertainment) held steady longer by leaning on steady slot machine play from locals. What's interesting is how international exposure buffered some, like LVS which drew from Macau's growth even as Vegas struggled, allowing it to cut dividends by 50% rather than eliminate them outright.

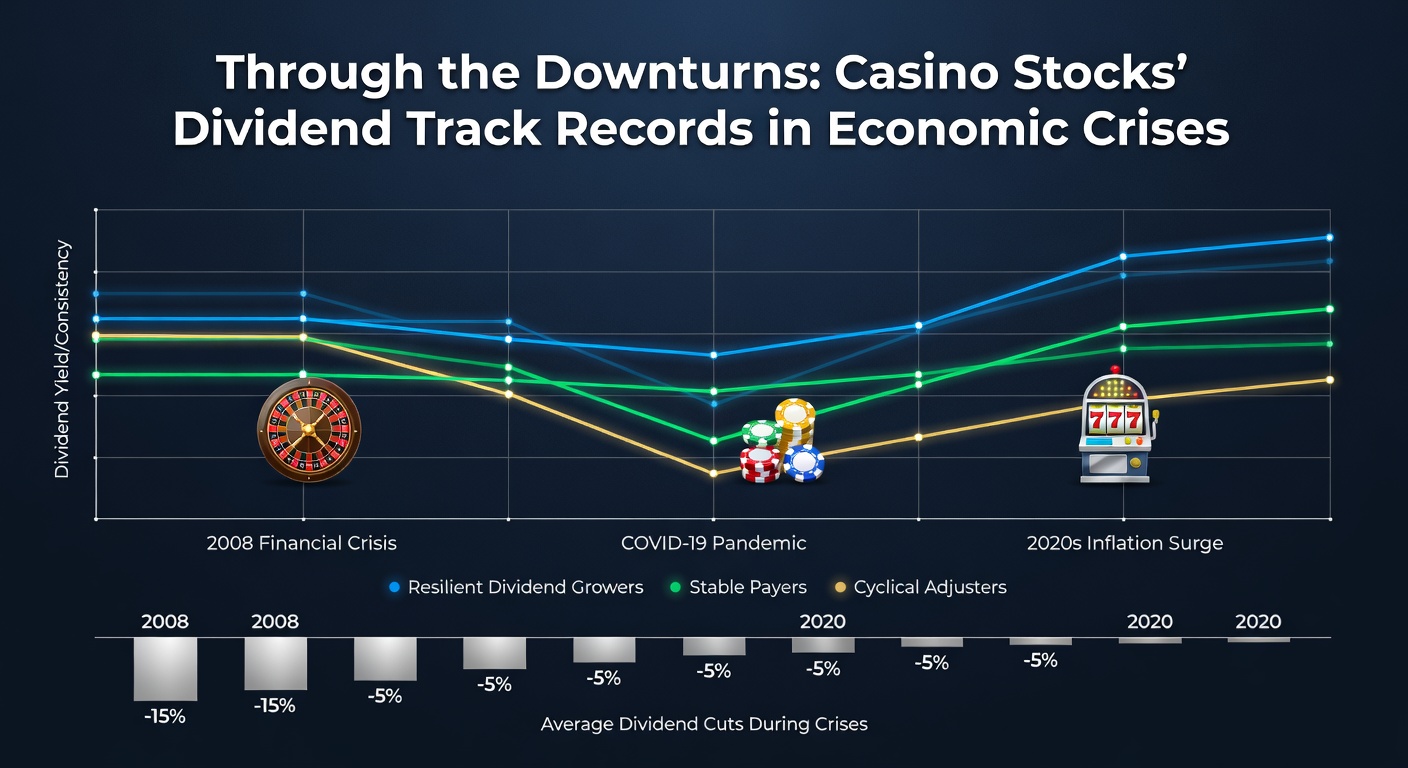

2008 Financial Crisis: A Dividend Stress Test

The subprime meltdown triggered widespread belt-tightening, and casino stocks dropped an average of 70% from peak to trough according to S&P data; MGM slashed its quarterly dividend from $0.25 to zero by mid-2009, prioritizing $12 billion in debt refinancing, while WYNN held its $0.25 payout through 2008 before halting it as EBITDA tumbled 40%. Researchers who've pored over SEC filings point out that LVS, despite Macau offsets, reduced yields from 3% to under 1% to fund Cotai Strip developments, a move that preserved operations but tested investor patience.

Smaller names showed resilience too; Churchill Downs Incorporated kept dividends flowing at $0.23 quarterly, buoyed by racetrack stability and Kentucky Derby draw, even as stock prices halved. But here's the thing: post-crisis recovery varied wildly, with companies that suspended payouts rebounding faster once Vegas conventions returned, data indicates dividends resumed by 2010 for most, often at higher rates thanks to pent-up demand.

COVID-19: The Ultimate Lockdown Challenge

Pandemic shutdowns in 2020 hammered the sector harder than 2008, with global GGR plunging 60-80% as casinos worldwide closed for months; Caesars Entertainment, fresh from its Eldorado merger, eliminated its nascent dividend immediately, while VICI Properties—the REIT spinning off casino real estate—held firm at $0.34 quarterly since it collects rents regardless of operations. Figures from the American Gaming Association reveal U.S. commercial gaming revenue cratered to $3.7 billion in Q2 2020 from $11.5 billion prior, prompting WYNN to suspend indefinitely and MGM to follow suit amid $4 billion cash burn.

Turns out, operators with strong balance sheets or digital pivots weathered better; DraftKings and Flutter Entertainment, though not traditional casinos, maintained or initiated dividends post-recovery by tapping online sports betting surges, a trend that persisted into 2021 reopenings. International players like Genting Singapore cut yields 75% but never zeroed out, supported by Resorts World Sentosa's domestic recovery; those who've studied balance sheets observe that debt-to-EBITDA ratios exceeding 5x correlated directly with full suspensions, whereas lower leverage allowed trims over cuts.

Other Downturns and Patterns Emerge

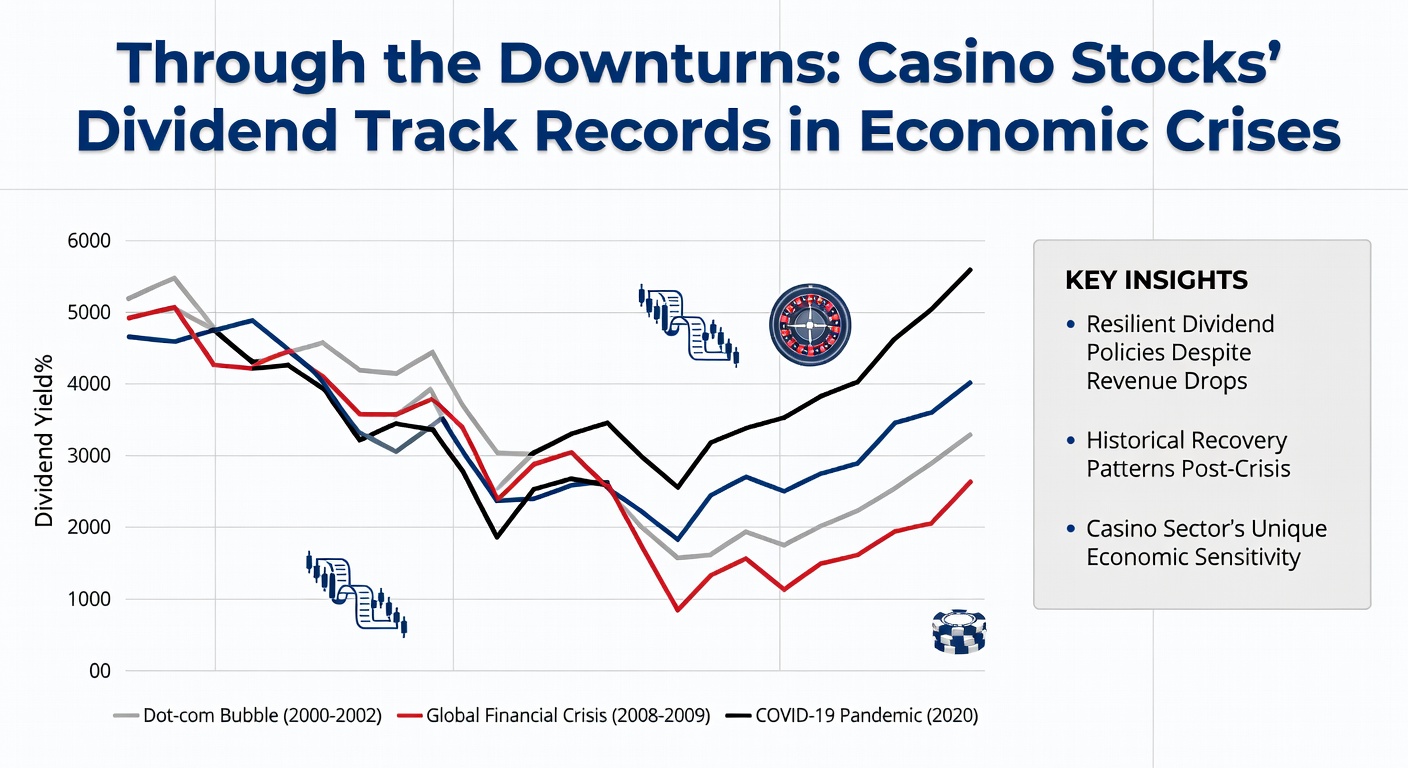

Beyond the big two, earlier shocks like the 2001 dot-com bust and post-9/11 slump tested the waters; Park Place Entertainment (pre-Caesars merger) trimmed dividends modestly as Vegas visitor counts fell 15%, yet quickly restored them with blackjack table expansions. Australian counterparts, such as Crown Resorts, faced their own 2009 hiccup with a 20% yield drop amid mining slowdowns, per company annual reports, but Macau fever soon overshadowed it.

Patterns across crises show dividends act as early warning signals; companies suspending during 2008 took 18 months on average to reinstate versus 12 for trimmers, research from gaming analysts uncovers, and those with diversified revenue—like tribal casinos or online arms—cut less severely. So, observers track payout ratios closely, noting anything over 80% pre-crisis flags vulnerability, while free cash flow coverage above 1.5x sustains them through storms.

Key Players' Track Records Side by Side

Lay out the scorecard, and Las Vegas Sands stands out for consistency; through 2008 it halved payouts but resumed aggressively by 2011 at $0.36 quarterly, riding Macau's 30% annual GGR growth, whereas MGM's zero-for-five-years suspension post-2008 and again in 2020 drew criticism yet enabled $10 billion capex for sportsbooks. Wynn toggles switches sharply—full stops in crises, then 4% yields in booms—reflecting its luxury focus vulnerable to high-rollers vanishing.

Regional stalwarts like Boyd Gaming shine quieter; they suspended briefly in 2009 and 2020 but reinstated faster, now at $0.16 quarterly with a 50-year no-cut streak for some subsidiaries, data shows. Melco Resorts, Asia-heavy, trimmed 90% in COVID but never eliminated, buoyed by Philippine and Cyprus venues; that's where geographic diversity pays off, as experts observe, blending Vegas volatility with steadier Asian play.

And don't overlook REITs like VICI and Gaming and Leisure Properties (GLPI); they hiked dividends 8% annually through 2020 chaos since triple-net leases guarantee flows, turning crises into yield havens for income seekers.

April 2026 Context: Echoes of Resilience

Fast forward to April 2026, and softening U.S. consumer spending amid inflation echoes past downturns, with Nevada GGR up just 2% year-over-year per preliminary state data, yet most majors hold dividends steady—MGM at $0.01 quarterly post-2022 reinstatement, LVS targeting hikes if EBITDA hits $7 billion. Australia's Crown Resorts navigates regulatory scrutiny while maintaining AUD 0.10 semi-annual, and Europe's Entain reports stable online yields despite retail dips.

Current filings suggest payout ratios hover at 40-60%, comfortable buffers against slowdowns, although analysts watch Macau's VIP recovery closely since it drives 40% of LVS profits. It's noteworthy that online gaming expansions—now 20% of U.S. revenue—provide ballast, much like they did post-COVID, keeping dividends intact even as physical floors see lighter traffic.

Conclusion

Through every downturn from 2001 slumps to 2020 lockdowns, casino stocks' dividend histories paint a picture of adaptability over fragility; while suspensions grab headlines, the majority trim and rebound stronger, with data underscoring that diversified operators and prudent leverage emerge unscathed. Researchers highlight that tracking free cash flow and geographic spreads reveals the sturdiest payers, a lesson holding firm into April 2026's cautious landscape. Those poring over charts know the rubber meets teh road in cash preservation, ensuring shareholders see returns when crowds return.